Why backtest your risk

Most traders pick risk limits arbitrarily ("I'll risk 1% per trade"). The Historical Risk Simulator answers whether that number is actually right for your strategy by replaying your real history against the rule you want to test.

Important: the system is a monitor, not an executor. It will not automatically close positions on the exchange — it alerts you when you deviate from your plan, so you build discipline yourself. For the general concept of risk control, see Learn: Risk Management.

The Risk Management section: a research lab for your trading discipline.

Risk Management, /app2/account/risk-management. Reused from _media/risk-management-v2/rm_overview (Mar 2026 rewrite).

Step 1 — Choose your scope

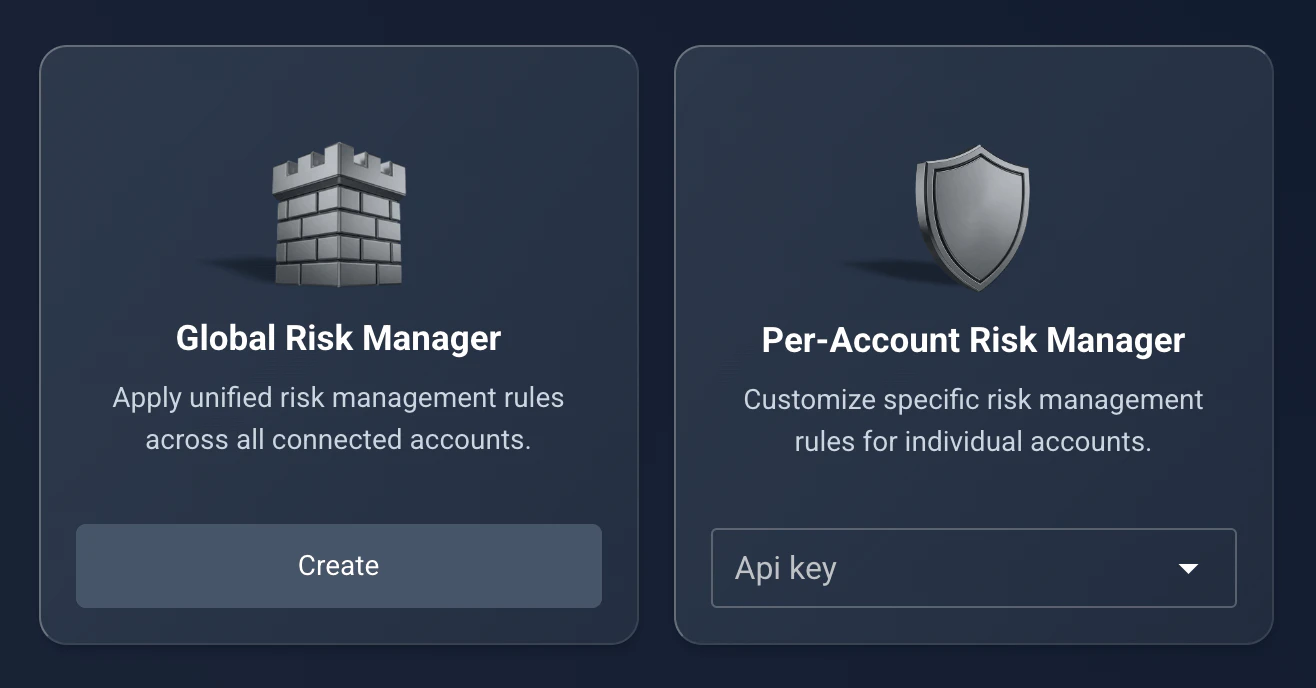

You can test rules at two levels:

- •Global Risk Manager — how the rules would affect your entire portfolio combined.

- •Per-Account Risk Manager — test specific strategies on specific sub-accounts (a tight stop on your "Scalping" account, a looser one on "Swing").

Step 1: choose Global or Per-Account scope.

Backtester scope select, /app2/account/risk-management/backtest. Reused from _media/risk-management-v2/backtest_step1 (Mar 2026); labels match riskManagement/locales/en.ts.

Step 2 — Define your hypothesis

Enter the limits you want to test — you do not need to enable them, just simulate. Common questions the backtester answers:

- •Max Loss Per Trade — "if I had cut every loser at −$50, how much would I have saved?"

- •Max Daily Loss — "if I had stopped after losing 2% in a day, would I have avoided the revenge-trading spiral?"

- •Max Leverage — "did high leverage actually increase my profit, or just my fees and losses?"

Step 2: enter the limits to test — max loss per trade, max daily loss, max leverage.

Backtester input parameters. Reused from _media/risk-management-v2/backtest_input (Mar 2026).

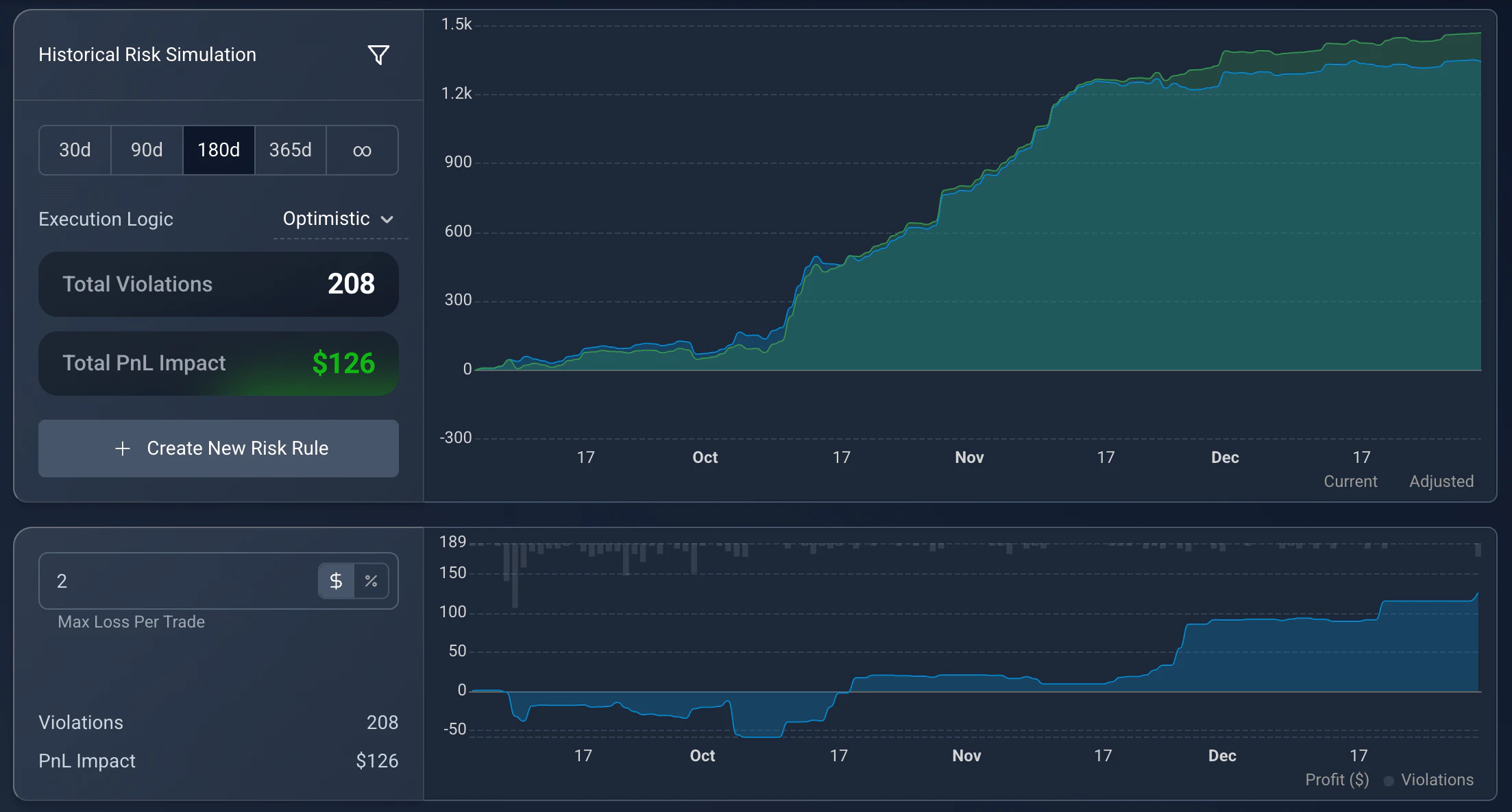

Step 3 — Read the simulation

Click Run Backtest and the system analyzes every trade you have made. The graph overlays two curves: the blue area is your actual PnL, and the green line is your equity curve if you had followed the rules.

If the green line is much lower than the blue, you are often "sitting through" losses — letting a trade go deep red before it recovers into profit. A strict limit cuts those recoveries, which shows as a vertical drop. Click a point to see which day caused the divergence.

Step 3: the blue area is your actual PnL; the green line is your equity curve under the rules.

Backtester results graph. Reused from _media/risk-management-v2/backtest_overview (Mar 2026).

Optimistic vs Realistic execution

This setting decides how the simulator handles the trade that breaks your daily limit:

- •Optimistic — assumes you cut the loss exactly at your limit (daily limit −$500, you exit at exactly −$500). This assumes perfect execution.

- •Realistic — records the entire loss of the trade that broke the limit, then ignores all later trades that day.

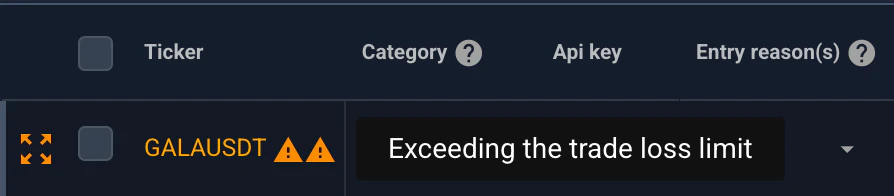

Trades that violated a rule are marked with a yellow warning icon.

My Trades list, violation marker. Reused from _media/risk-management-v2/trades_list_example_violation (Mar 2026).

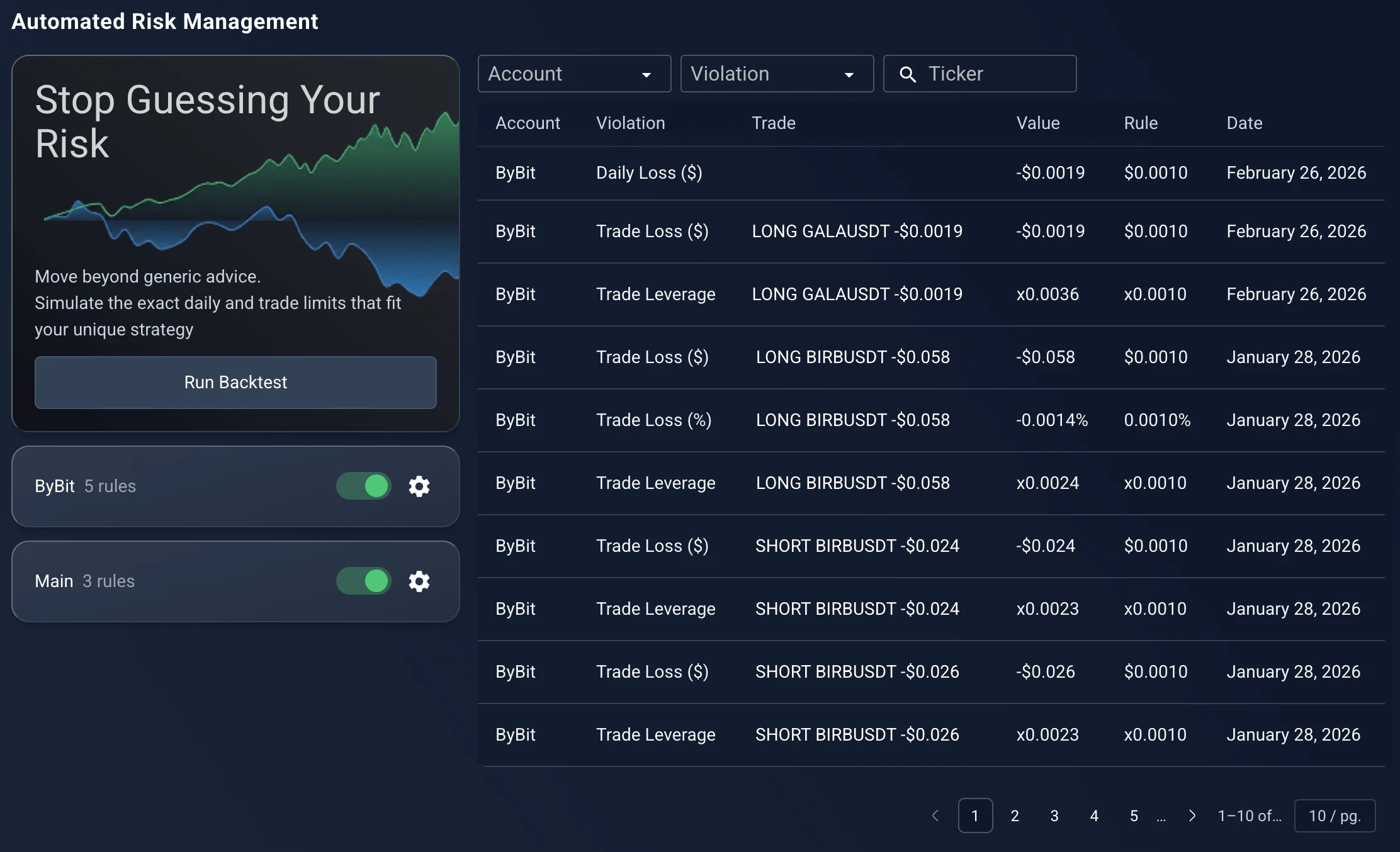

Active monitoring & alerts

When you enable a rule, the app monitors your trades in real time and logs every violation — it does not block you, it keeps you accountable. Click any violation to see the specific trade that caused it.

Connect a Telegram or Discord connection to receive instant alerts (for example "⚠️ Daily Loss Limit Exceeded: −$505, Limit: −$500"). In the app, trades that violated a rule are marked with a yellow warning icon.